Employer-sponsored health insurance remains the foundational pillar of the United States healthcare system, serving as the primary source of medical coverage for the vast majority of Americans under the age of 65. As of March 2025, new data indicates that approximately 165.6 million individuals rely on their employers or a family member’s employer for health insurance. This figure underscores the enduring central role of the private sector in financing healthcare, yet a closer examination of the data reveals a landscape characterized by profound inequities and systemic barriers to access. While the aggregate number of covered lives remains high, the reach of these benefits is increasingly uneven, shaped largely by income levels, industry types, and the specific eligibility criteria set by employers.

The latest analysis from the Peterson-KFF Health System Tracker, based on the Annual Economic and Social (March) Supplements of the Current Population Survey, highlights a persistent "coverage chasm." While roughly 80% of all adult workers under age 65 are employed by firms that offer health insurance to at least a portion of their workforce, this availability is not distributed equally across the economic spectrum. For lower-paid workers, the likelihood of being offered coverage drops significantly to just 60%. This 20-point disparity marks a critical point of failure in the traditional employer-based model, where those with the least financial flexibility are also the least likely to have access to the most common form of risk protection.

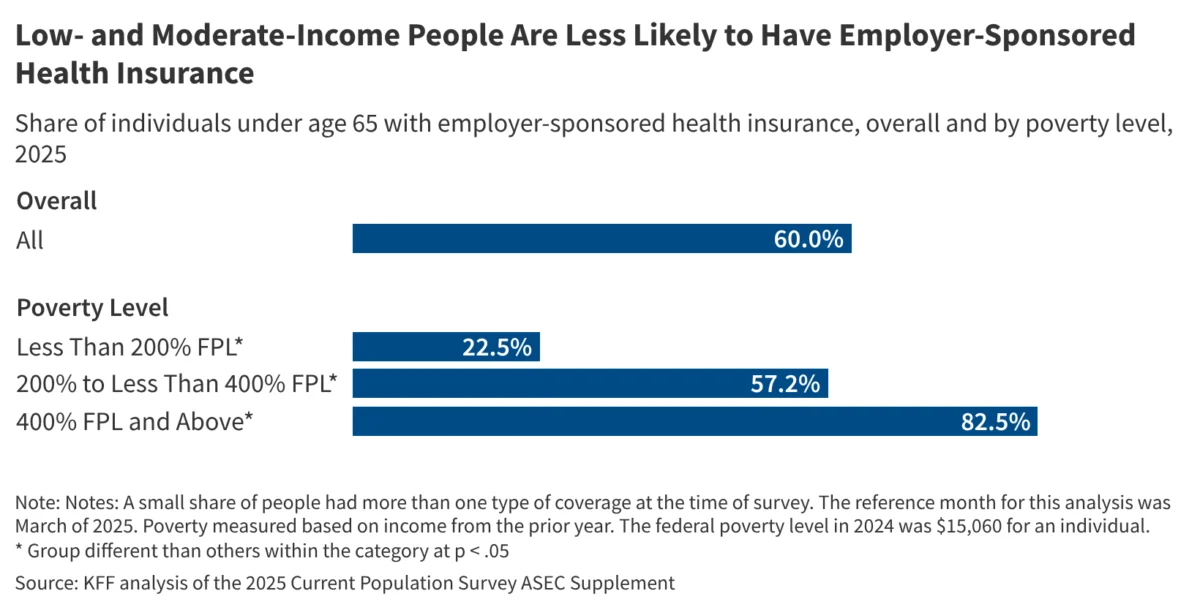

The Income Divide in Coverage and Enrollment

The disparities in employer-sponsored insurance (ESI) are not merely a matter of whether a company offers a plan, but also whether the employees can afford to participate in it. The data shows that even when coverage is available, enrollment rates fluctuate wildly based on household income. Among individuals under age 65 living in households with incomes below 200% of the federal poverty level, only 22.5% are covered by employer-sponsored insurance. In stark contrast, 82.5% of those with household incomes at or above 400% of the federal poverty level are enrolled in ESI.

This gap suggests that for the "working poor," the offer of insurance does not always equate to the possession of insurance. High premium contributions, rising deductibles, and the overall cost of living often force lower-income workers to waive coverage in favor of higher take-home pay, or they may find that they do not meet the hours-worked requirements to qualify for the plan. This phenomenon, often referred to as "opt-out" behavior due to unaffordability, creates a scenario where the lowest earners are left to navigate the complexities of Medicaid or the Affordable Care Act (ACA) marketplaces, or remain uninsured entirely.

A Historical Chronology of Employer-Sponsored Insurance

To understand the current state of ESI in 2025, it is necessary to look at the evolution of the American health benefit system over the last eight decades. The reliance on employers for health coverage was not a designed outcome but rather an accidental byproduct of wartime economic policy.

- The 1940s and the Stabilization Act: During World War II, the U.S. government imposed wage freezes to prevent inflation. To compete for labor, employers began offering health benefits, which were not considered "wages" and thus were exempt from the freeze. In 1943, the Internal Revenue Service (IRS) ruled that employer contributions to group health insurance were tax-exempt, a policy codified by Congress in 1954. This established the permanent tax advantage that still drives the ESI market today.

- 1974 – The ERISA Era: The Employee Retirement Income Security Act (ERISA) was passed, creating a federal framework for employer-provided benefits. This allowed large, multi-state corporations to self-insure and bypass varying state insurance mandates, further cementing the employer’s role as a primary health plan sponsor.

- 2010 – The Affordable Care Act (ACA): The ACA introduced the "employer mandate," requiring firms with 50 or more full-time equivalent employees to offer affordable coverage that meets minimum value standards or face financial penalties. While this stabilized offer rates in large firms, it did little to bridge the gap for small businesses or part-time workers.

- 2020-2023 – The Pandemic Shift: The COVID-19 pandemic highlighted the vulnerability of ESI, as millions lost coverage during brief periods of record unemployment. However, the subsequent "Great Resignation" and labor shortages forced many employers to enhance benefits to attract talent, leading to a temporary stabilization in coverage rates.

- 2024-2025 – The Post-Inflationary Landscape: By 2025, the cumulative impact of several years of high inflation has forced a reckoning. Employers are facing double-digit increases in healthcare costs, which they are increasingly passing on to employees through higher premiums and cost-sharing, disproportionately affecting the low-wage workforce.

Structural Barriers and the Role of Firm Size

The Peterson-KFF analysis points to firm size and industry as primary determinants of insurance availability. Large corporations (500+ employees) almost universally offer health benefits, often as part of a comprehensive "total rewards" package designed to retain high-skill labor. However, in the small business sector—particularly in the service, hospitality, and retail industries—the cost of administering a health plan can be prohibitive.

Lower-paid workers are statistically more likely to be employed by these smaller firms or in industries with high turnover rates. For these employers, the administrative burden and the high per-employee cost of small-group premiums create a significant barrier. Furthermore, the "gig economy," which has continued to expand through 2025, leaves millions of contractors and freelance workers outside the ESI umbrella entirely, as they are legally classified as self-employed rather than employees.

The Affordability Crisis and "Underinsurance"

Even for those counted among the 165.6 million with coverage, the quality of that coverage is a growing concern. The 2025 data suggests that "underinsurance" is becoming as significant a challenge as being uninsured. Underinsurance occurs when a person has health coverage, but the out-of-pocket costs (deductibles and co-pays) are so high relative to their income that they delay or forgo necessary medical care.

In 2025, the average annual premium for family coverage has reached new heights, often exceeding $25,000, with employers typically picking up about 70-75% of that cost. For a worker earning $40,000 a year, contributing $6,000 or $7,000 toward a premium—plus facing a $3,000 deductible—is financially untenable. This explains the massive discrepancy in enrollment between the 200% and 400% poverty levels. The system effectively functions well for the upper-middle class and wealthy but provides a diminishing return for those at the bottom of the pay scale.

Perspectives from Stakeholders and Policy Analysts

Industry experts and policy analysts have reacted to these findings with a mixture of concern and a call for structural reform. "The fact that 80% of workers are offered coverage is a testament to the resilience of the employer-based system," says Dr. Elena Rodriguez, a senior fellow at a prominent healthcare think tank. "But the 22.5% enrollment rate for low-income families is a flashing red light. We are seeing a system that works for the affluent but leaves the essential workforce in a state of perpetual medical insecurity."

Business advocacy groups argue that the rising costs are out of their control. "Employers want to provide the best possible benefits to their teams," a spokesperson for a national small business association stated. "However, with the cost of prescription drugs and hospital services skyrocketing, many small owners are forced to choose between offering a plan that no one can afford to use or not offering one at all. The tax incentives currently in place are simply not enough to offset the raw cost of care in 2025."

Broader Implications for the U.S. Healthcare System

The uneven distribution of employer-sponsored insurance has profound implications for the broader U.S. economy and public health. When 165.6 million people are covered by private plans, it relieves pressure on public programs like Medicaid and Medicare. However, the "coverage gap" for low-income workers puts a secondary strain on these programs. Many workers who are offered "unaffordable" ESI find themselves in a "subsidy cliff," where they earn too much for Medicaid but are ineligible for ACA marketplace subsidies because their employer’s offer is technically deemed "affordable" by government standards (even if it isn’t practically affordable for their specific budget).

This misalignment leads to several critical outcomes:

- Increased Emergency Room Utilization: Those without adequate coverage often delay primary care, leading to more expensive emergency interventions later.

- Labor Market Friction: The "job lock" phenomenon persists, where workers stay in positions they dislike solely to maintain health benefits, stifling entrepreneurship and economic mobility.

- Public Health Disparities: Chronic conditions like diabetes and hypertension go unmanaged in low-income populations who lack the ESI coverage their wealthier counterparts enjoy, leading to lower life expectancy and higher long-term disability rates.

Conclusion and Future Outlook

The March 2025 data from the Peterson-KFF Health System Tracker serves as a vital check-up on the health of the American insurance landscape. While employer-sponsored insurance remains the "gold standard" for 165.6 million people, the fragility of this model for the lower-income workforce is more apparent than ever. As the gap between the 22.5% and 82.5% enrollment rates illustrates, income remains the single greatest predictor of health security in the United States.

Looking forward, the debate over the future of healthcare is likely to focus on how to bridge this gap. Proposed solutions range from enhancing ACA subsidies for those with "unaffordable" employer offers to creating a "public option" that could compete with private plans. Until such systemic changes are implemented, the U.S. will continue to operate a two-tiered system where the quality of one’s health coverage is inextricably linked to the size of one’s paycheck. The 2025 figures confirm that while the employer-sponsored model is not disappearing, it is failing to adapt to the economic realities of the modern American worker.

{kind=link}