The high cost of health care remains a persistent and growing burden for families across the United States, frequently dictating critical decisions regarding insurance coverage and medical treatment. According to the latest comprehensive polling data from KFF, updated in April 2026, health care costs have solidified their position as the primary financial concern for American adults, surpassing other essential living expenses such as housing, groceries, and transportation. The data paints a stark picture of a nation where even those with health insurance are not shielded from the rising tide of medical inflation, leading to significant delays in care and a burgeoning crisis of medical debt.

The Affordability Crisis Across Demographics

While the struggle to afford medical care is a near-universal concern, the impact is felt most acutely by specific segments of the population. KFF polling indicates that 44% of all U.S. adults find it difficult to afford their health care costs. This figure, however, masks deep disparities based on insurance status, income, and race. For uninsured adults under the age of 65, the situation is dire, with 82% reporting difficulty in managing medical expenses.

Income levels also serve as a primary indicator of financial strain. Households earning less than $40,000 annually report the highest levels of difficulty, but the crisis is increasingly creeping into middle-income brackets. Furthermore, racial and ethnic disparities persist; 55% of Hispanic adults and 49% of Black adults report trouble affording care, compared to 39% of White adults. These statistics underscore a systemic challenge where the cost of staying healthy is becoming a luxury that many cannot consistently afford.

The trend of financial hardship has shown a steady trajectory over the past several years. When looking specifically at the 12 months leading into 2026, approximately 28% of adults reported that they or a family member had direct problems paying for care. This number spikes to 41% among Hispanic households and 40% among young adults aged 18 to 29, suggesting that the youngest generation of workers is facing a particularly steep climb in the current economic landscape.

The Dangerous Choice: Skipping Care Due to Costs

One of the most concerning outcomes of high medical costs is the "rationing" of care by patients themselves. Approximately one-third of U.S. adults (36%) admit to skipping or postponing needed health care services in the past year solely because of the cost. This behavior is not limited to those without coverage; 37% of insured individuals also reported delaying care for financial reasons, highlighting a phenomenon often referred to by policy experts as "underinsurance," where coverage exists but out-of-pocket requirements remain prohibitive.

The gender gap in this area is also notable, with 38% of women reporting skipped care compared to 32% of men. This disparity often stems from the fact that women frequently manage the health care needs of their households and may prioritize the care of children or partners over their own. Conversely, adults aged 65 and older—most of whom are covered by Medicare—are significantly less likely to skip care, demonstrating the relative stability provided by universal social insurance programs for seniors.

However, the consequences of delayed care are not merely financial; they are physiological. Nearly 20% of adults report that their health worsened specifically because they postponed or skipped a medical visit or treatment. Among the uninsured, this figure doubles to 42%. By the time these individuals eventually seek care, their conditions are often more advanced, requiring more intensive and expensive interventions, which further exacerbates the cycle of medical debt and health decline.

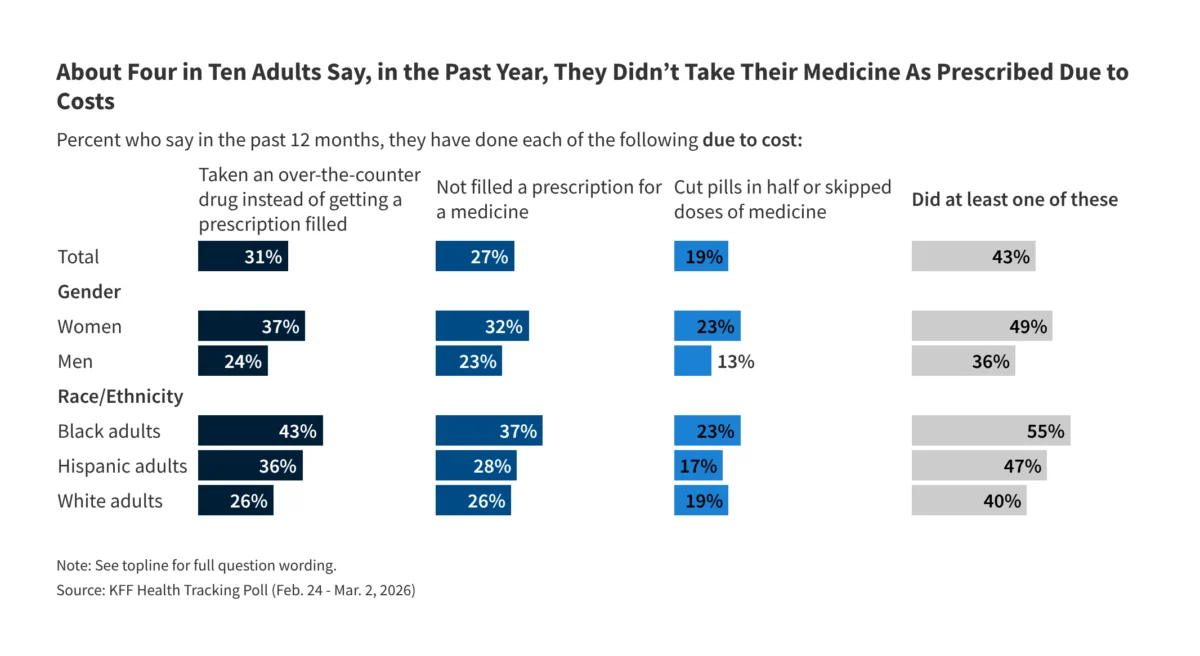

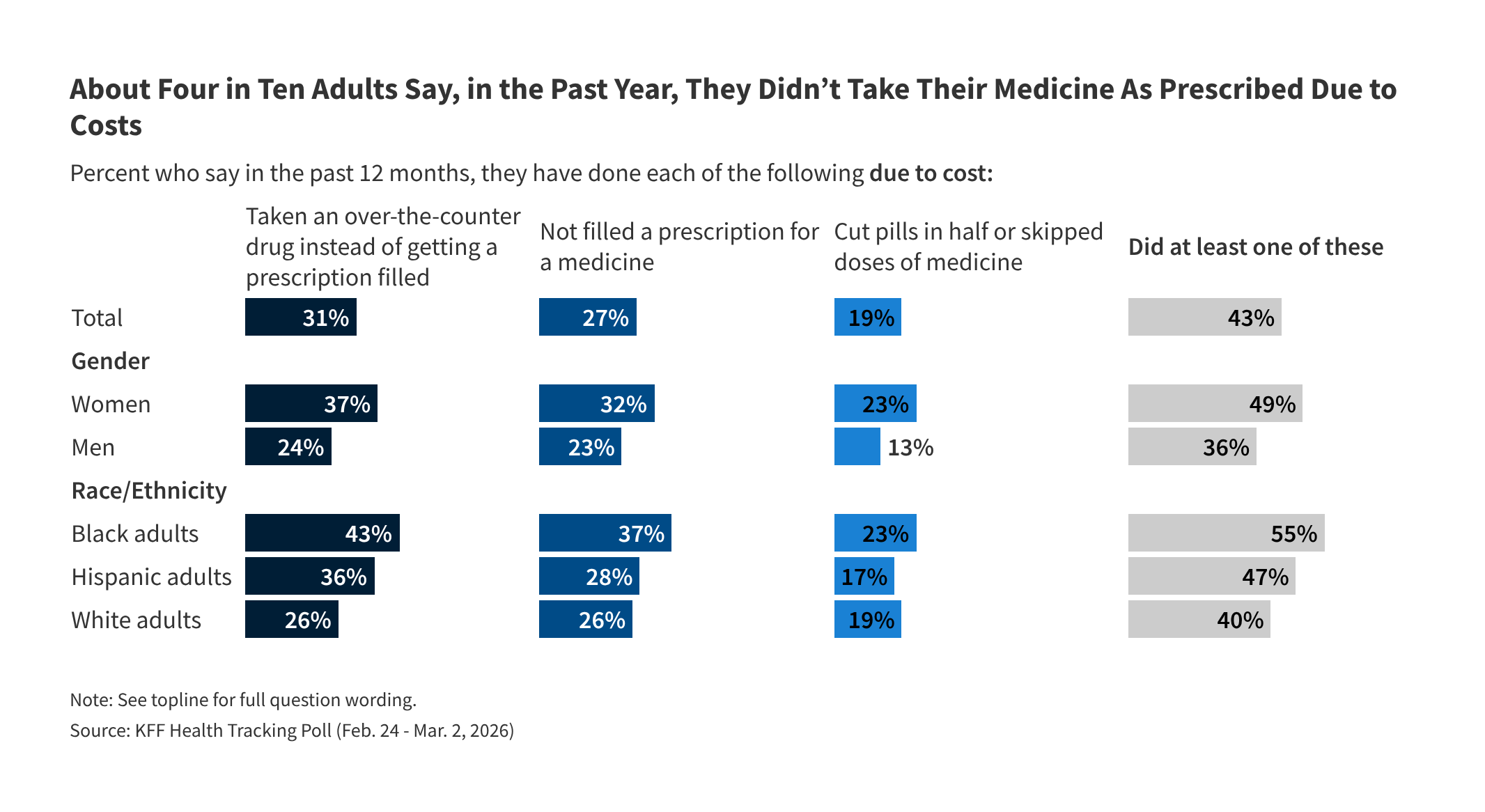

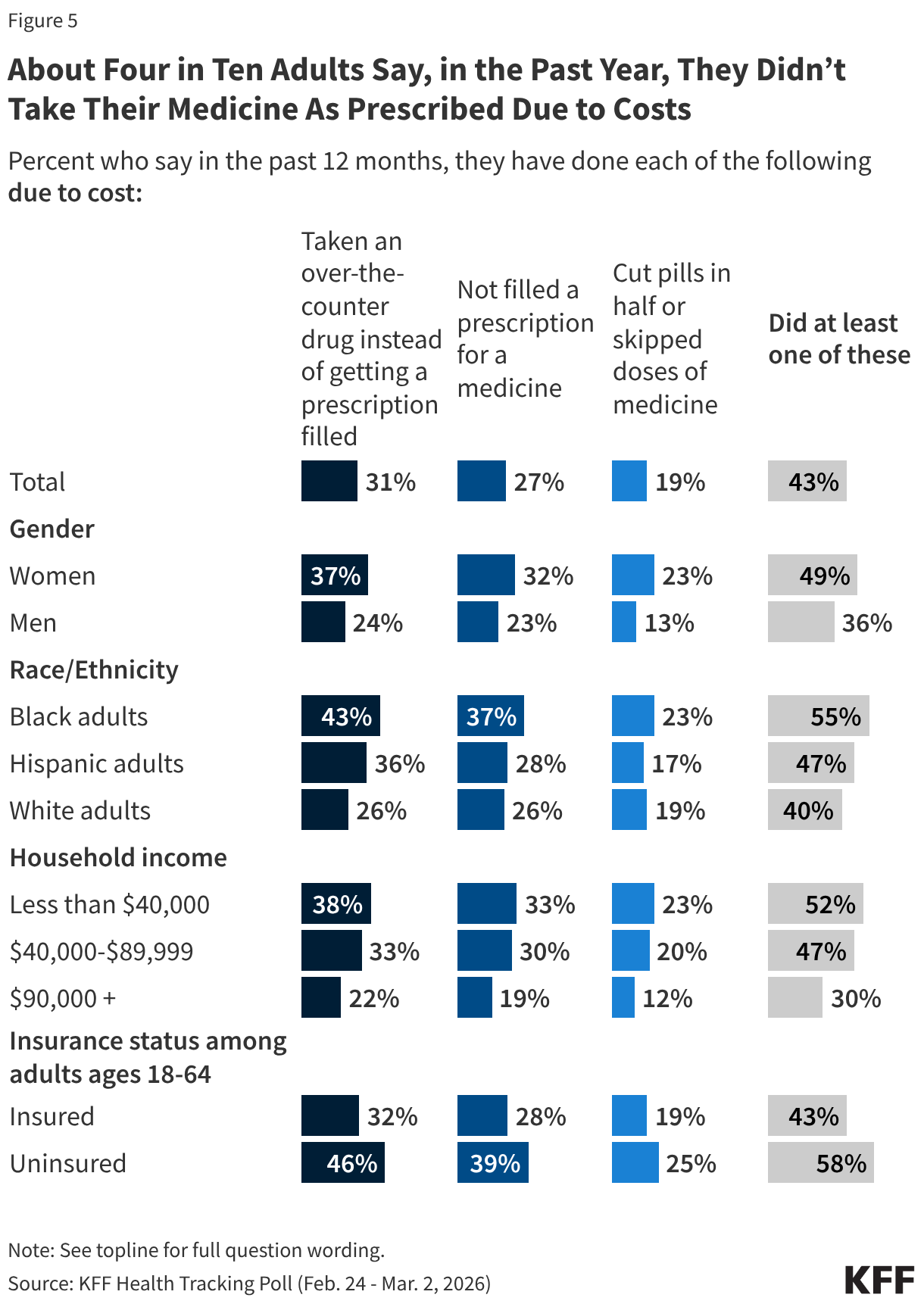

The Escalating Cost of Prescription Medications

Prescription drug affordability has emerged as a major flashpoint in the American health care debate. As of March 2026, 43% of adults reported taking at least one measure to reduce the cost of their medications, a significant increase from 33% in 2025 and 31% in 2023. These measures include taking over-the-counter alternatives (31%), leaving prescriptions unfilled (27%), or dangerously cutting pills in half and skipping doses (19%).

The burden of drug costs is particularly heavy on Black adults (55%) and women (49%). Furthermore, over half of adults in households earning less than $40,000 annually report non-adherence to prescribed medication schedules due to cost. Policy analysts suggest that while recent legislative efforts have sought to cap costs for certain medications, the broader market continues to see price increases that outpace wage growth, leaving many families to choose between their prescriptions and other necessities.

The Illusion of Protection: Insurance Ratings and Out-of-Pocket Realities

While health insurance is designed to provide financial security, many Americans view their current plans as inadequate. While a majority of insured adults rate their plans as "good" or "excellent," a significant minority—at least 30%—rate their insurance as "fair" or "poor" regarding monthly premiums and out-of-pocket costs for doctor visits and prescriptions.

Dissatisfaction is highest among those with private insurance, whether through an employer or the Affordable Care Act (ACA) Marketplace. These individuals are more likely to face high deductibles and co-pays compared to those on Medicaid or Medicare. Medicaid enrollees typically report the highest satisfaction with affordability, largely because the program limits or eliminates premiums and out-of-pocket costs for low-income participants. This suggests that the "private-sector" model of health coverage in the U.S. is increasingly failing to meet the public’s expectations for affordability.

The Growing Crisis of Medical Debt

Medical debt has become a structural feature of the American economy. A landmark investigation and subsequent KFF survey found that 41% of U.S. adults currently carry some form of debt due to medical or dental bills. This includes 24% who have bills that are past due and 21% who are paying off providers over time.

The reach of this debt is extensive:

- 17% of adults owe money to banks or collection agencies for medical loans.

- 17% have put medical bills on credit cards that they are paying off over time.

- 10% have borrowed money from family or friends to cover health care costs.

This "debt trap" creates a compounding effect. Individuals already in medical debt are 51% more likely to skip future medical tests or treatments recommended by a doctor, fearing further financial ruin. This creates a permanent class of "medical debtors" who are effectively locked out of the health care system despite having ongoing medical needs.

Financial Fragility and Unexpected Expenses

The fragility of the American household’s finances is perhaps most clearly seen in the "unexpected bill" test. Approximately 50% of U.S. adults say they would be unable to pay an unexpected medical bill of $500 out of pocket. Within this group, 19% say they could not pay the bill at all, while the remainder would have to borrow money or incur high-interest credit card debt.

This lack of a financial cushion is a major driver of the "worry" that dominates the public consciousness. As of early 2026, 66% of adults are "somewhat" or "very" worried about affording health care. To put this in perspective, this level of concern is higher than the worry associated with paying for food (57%), utilities (57%), or housing (52%). For the American public, a medical emergency is no longer just a health crisis; it is viewed as a primary threat to their overall financial survival.

Long-Term Care: The Looming Anxiety for Aging Americans

As the "Baby Boomer" generation continues to age, the cost of long-term care has become a source of intense anxiety. Nearly 60% of adults aged 65 and older express fear about affording nursing home care or assisted living. Among those aged 50 to 64—the group currently approaching retirement—the anxiety is even higher, with over 70% worried about affording residential care or home health aides.

The U.S. system for long-term care is often described as a "patchwork" that requires individuals to spend down nearly all their assets to qualify for Medicaid assistance, as Medicare does not cover most long-term custodial care. This looming financial cliff is a significant stressor for middle-class families who fear that their life savings will be entirely consumed by a few years of specialized care.

Broader Implications and Policy Analysis

The data provided by KFF suggests that the American health care system is reaching a tipping point. The fact that health care costs now outrank housing and food as a primary financial concern indicates that the current mechanisms for controlling costs—such as high-deductible health plans and managed care—are not providing the relief consumers need.

From a public health perspective, the trend of skipping care and medications suggests a future of higher chronic disease rates and increased emergency room utilization, which are ultimately more expensive for the system as a whole. From a political perspective, these findings are likely to play a central role in the 2026 midterm elections. Candidates across the spectrum will likely face pressure to address not just the "access" to insurance, but the "affordability" of the care that insurance is supposed to provide.

The persistent disparities among Black and Hispanic populations also highlight that health care cost is a civil rights issue. Without targeted interventions to lower out-of-pocket burdens for these communities, the gap in health outcomes is likely to widen.

In conclusion, while the United States remains a global leader in medical innovation and technology, the KFF data reveals a fundamental disconnect: the fruits of that innovation are increasingly out of reach for a significant portion of the population. As medical debt becomes a standard part of the American experience, the call for systemic reform—whether through enhanced subsidies, direct price negotiations, or expanded public options—is likely to grow louder, driven by a public that feels increasingly vulnerable to the high cost of simply staying alive.

{kind=link}