As of 2025, employer-sponsored health insurance (ESI) remains the foundational pillar of the American healthcare system, serving as the primary source of coverage for approximately 165.6 million residents under the age of 65. Unlike most developed nations that rely on universal or state-funded healthcare, the United States continues to utilize a voluntary, private-sector model where the workplace serves as the central hub for medical benefits. While this system offers administrative efficiencies and significant tax advantages, recent data from 2025 highlights a growing disparity in coverage quality and accessibility, particularly for low-wage workers and those employed by smaller firms.

The Structural Framework of Employment-Based Coverage

Employer-sponsored health insurance is a form of group health insurance where a sponsoring entity—typically a private employer, a union, or a trade association—offers medical benefits to its workforce and their dependents. This system is distinct from the individual or non-group market, where consumers purchase policies directly from insurers or through government-regulated exchanges like Healthcare.gov.

In the ESI landscape, employers generally utilize one of two funding mechanisms. Under an "insured plan," the employer pays premiums to a state-licensed health insurance company, which then assumes the financial risk of medical claims. Conversely, many large corporations opt for "self-funded plans," where the employer pays for healthcare services directly from its own assets. To mitigate the risk of catastrophic costs, self-funded employers often purchase stop-loss insurance. According to 2025 data, the majority of large-scale employers favor self-funding as it provides greater control over plan design and cash flow.

The legal backbone of this system is the Employee Retirement Income Security Act of 1974 (ERISA). This federal law establishes the standards for disclosure, fiduciary responsibility, and fair dealing for private-sector employee benefit plans. While ERISA provides a cohesive national framework, it notably does not apply to plans offered by government entities or churches, which are governed by different sets of regulations.

A Historical Chronology: From Wartime Necessity to Market Dominance

The dominance of ESI in the United States was not an intentional design by health policy architects but rather an evolution of wartime economic policy and subsequent tax legislation.

- 1942: The War Labor Board Decision. During World War II, the federal government imposed strict wage freezes to prevent inflation. To attract and retain talent in a competitive labor market, employers began offering "fringe benefits," including health insurance, which were not counted as wages.

- 1954: Internal Revenue Code Codification. The U.S. Congress formally enshrined the tax-exempt status of employer-sponsored health benefits. This meant that employer contributions toward health premiums were excluded from an employee’s taxable income.

- 1974: The Passage of ERISA. Federal oversight was established to protect workers’ benefits and ensure transparency in how plans were managed.

- 2010: The Affordable Care Act (ACA). The ACA introduced the "employer mandate," requiring firms with 50 or more full-time equivalent employees (FTEs) to offer affordable, high-value coverage or face financial penalties.

- 2023-2024: The "Family Glitch" Correction. New federal rules addressed a long-standing loophole where affordability was only measured by the cost of individual coverage, often leaving family dependents ineligible for marketplace subsidies despite high costs.

The Economic Engine: Tax Exclusions and Market Efficiencies

The persistence of ESI is driven by two primary economic factors: tax advantages and administrative efficiency. The exclusion of health insurance premiums from federal income and payroll taxes represents one of the largest "tax expenditures" in the U.S. budget. In 2022, this exclusion cost the federal government approximately $312 billion in foregone revenue.

From the perspective of an employee, a dollar of health benefits is more valuable than a dollar of wages. For a worker in a 22% marginal tax bracket with standard payroll taxes, an employer would need to pay nearly $1.38 in wages to provide the same purchasing power as $1.00 in tax-free health insurance.

Furthermore, the workplace provides a natural hedge against "adverse selection." In the individual market, those with high medical needs are the most likely to seek insurance, which can drive up premiums. In contrast, people generally choose jobs based on their skills and the nature of the work, not their health status. This provides insurers with a balanced risk pool of healthy and unhealthy individuals, lowering the overall cost of premiums.

2025 Coverage Data and Demographic Disparities

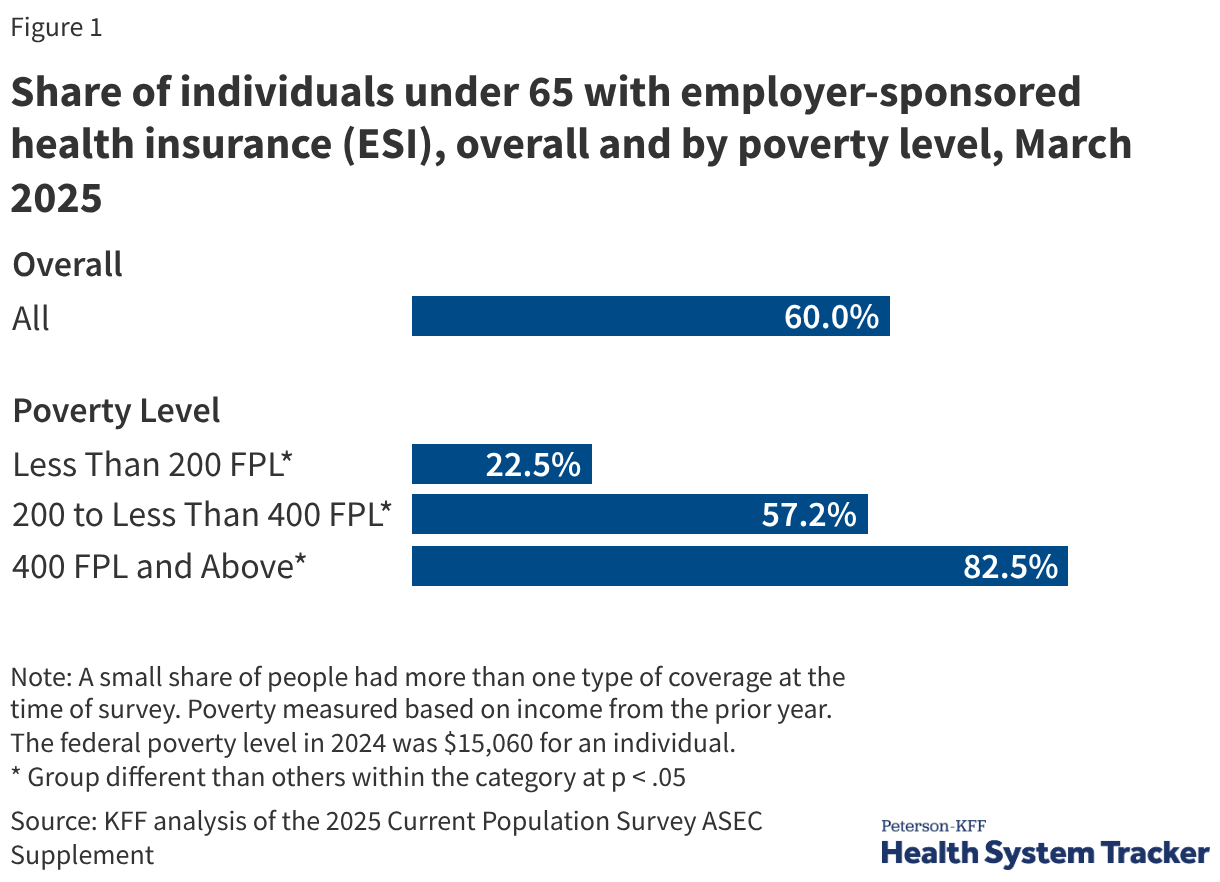

Recent findings from March 2025 indicate that 60% of Americans under age 65 are covered by ESI. However, this figure masks significant inequities across different socio-economic and demographic lines.

Income and Eligibility

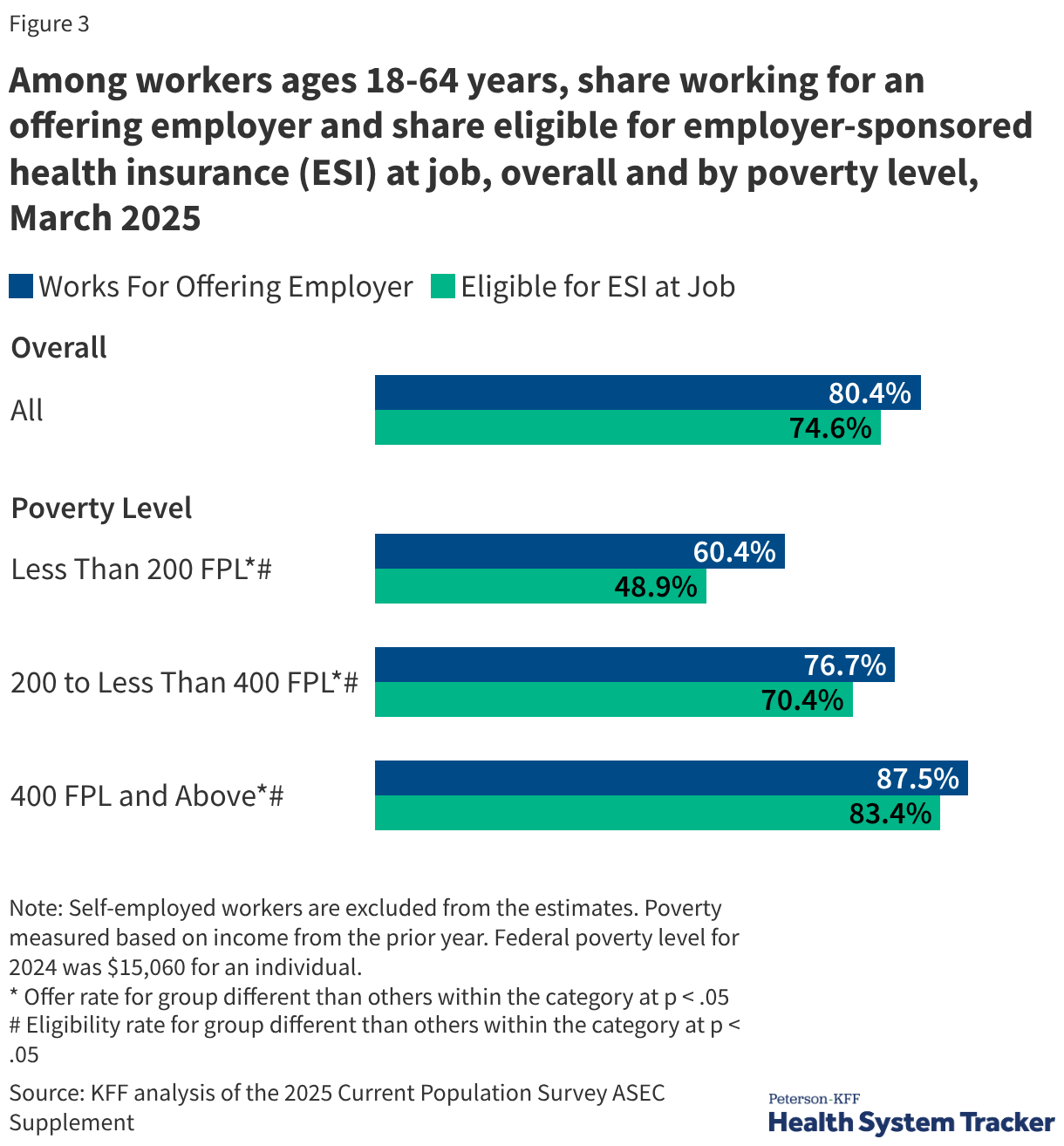

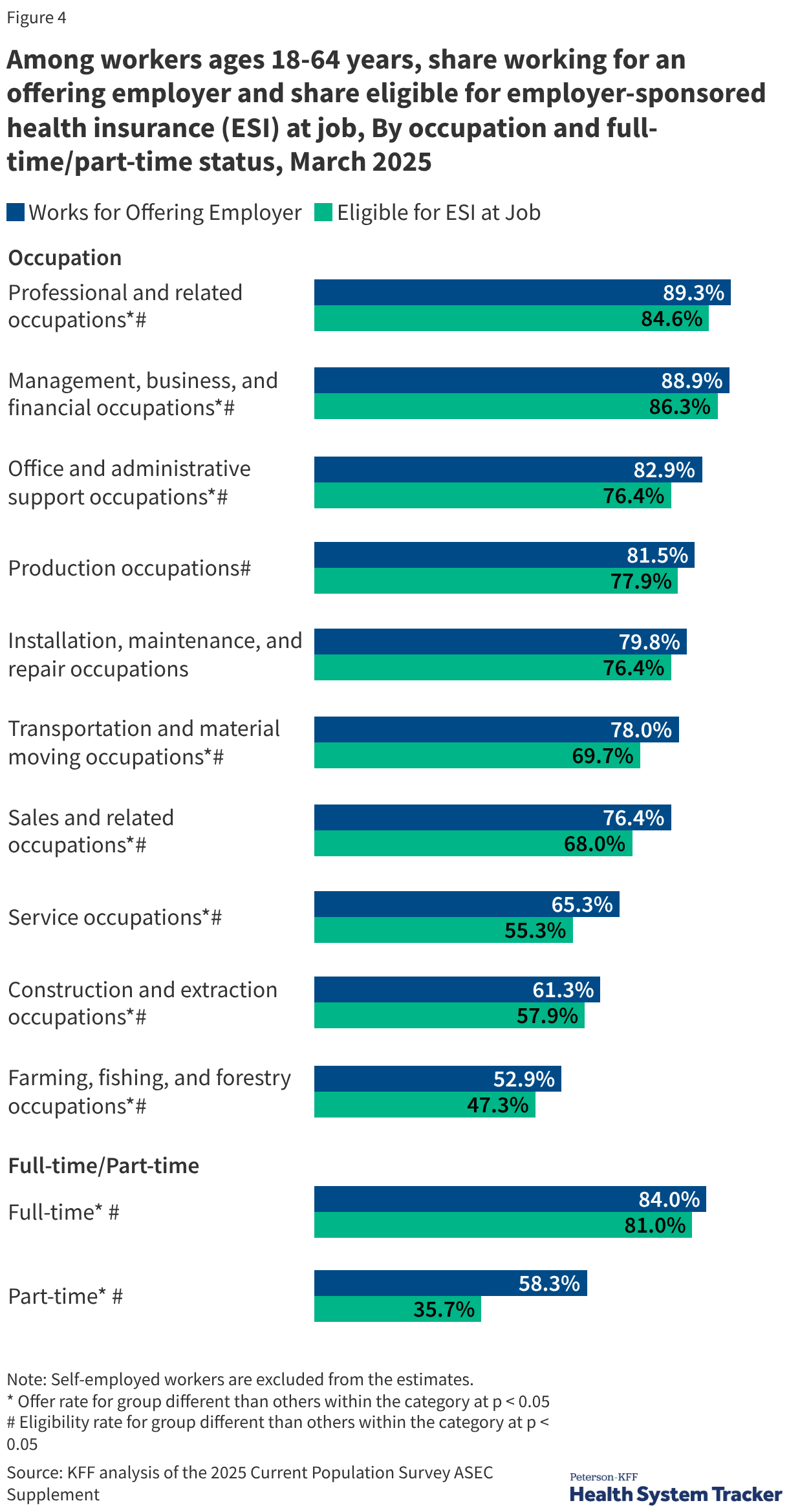

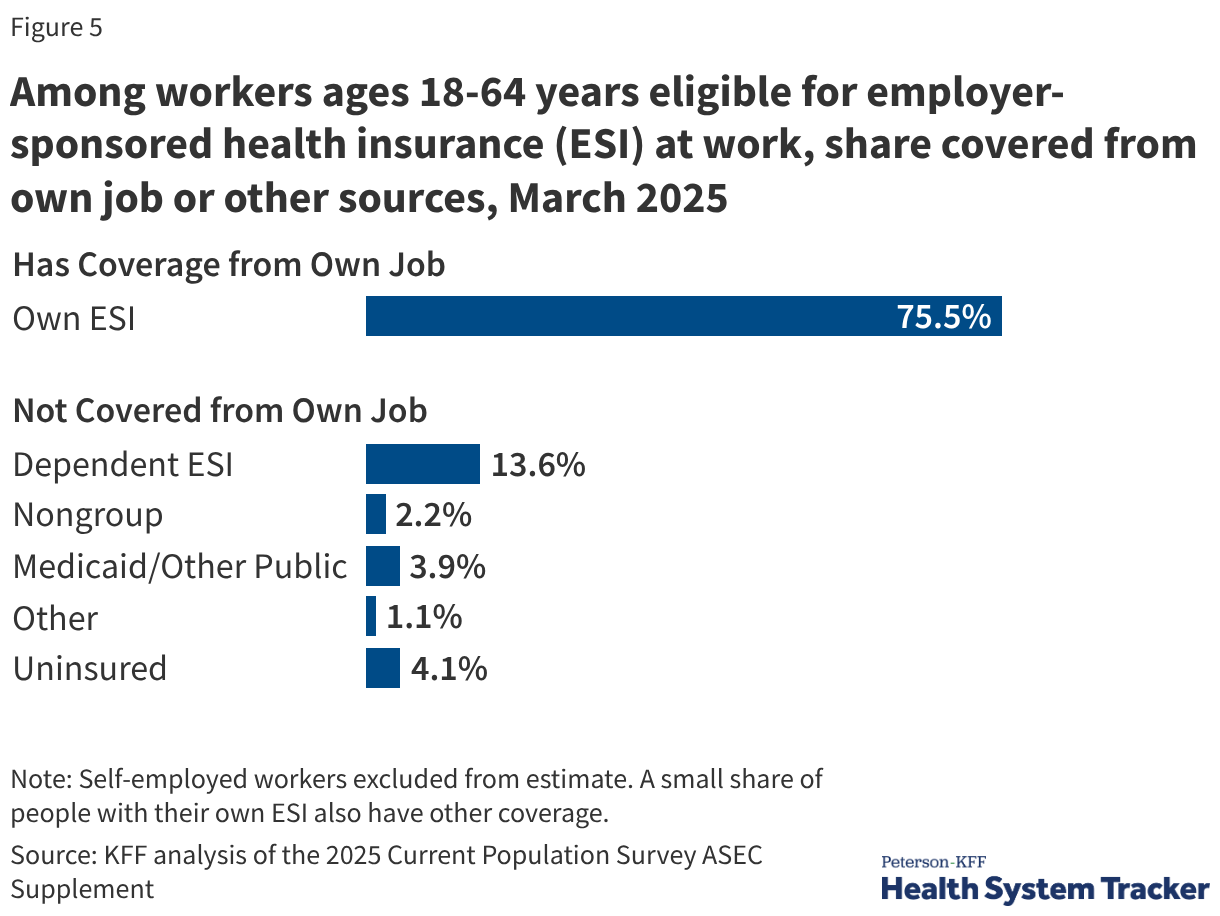

Coverage rates are inextricably linked to household income. Among adults under 65 with incomes at or above 400% of the federal poverty level (FPL), 82.5% have ESI. In stark contrast, only 22.5% of those with incomes below 200% of the FPL are covered through an employer. This gap is driven by both lower "offer rates" from low-wage employers and lower eligibility rates for part-time or seasonal workers.

Race and Ethnicity

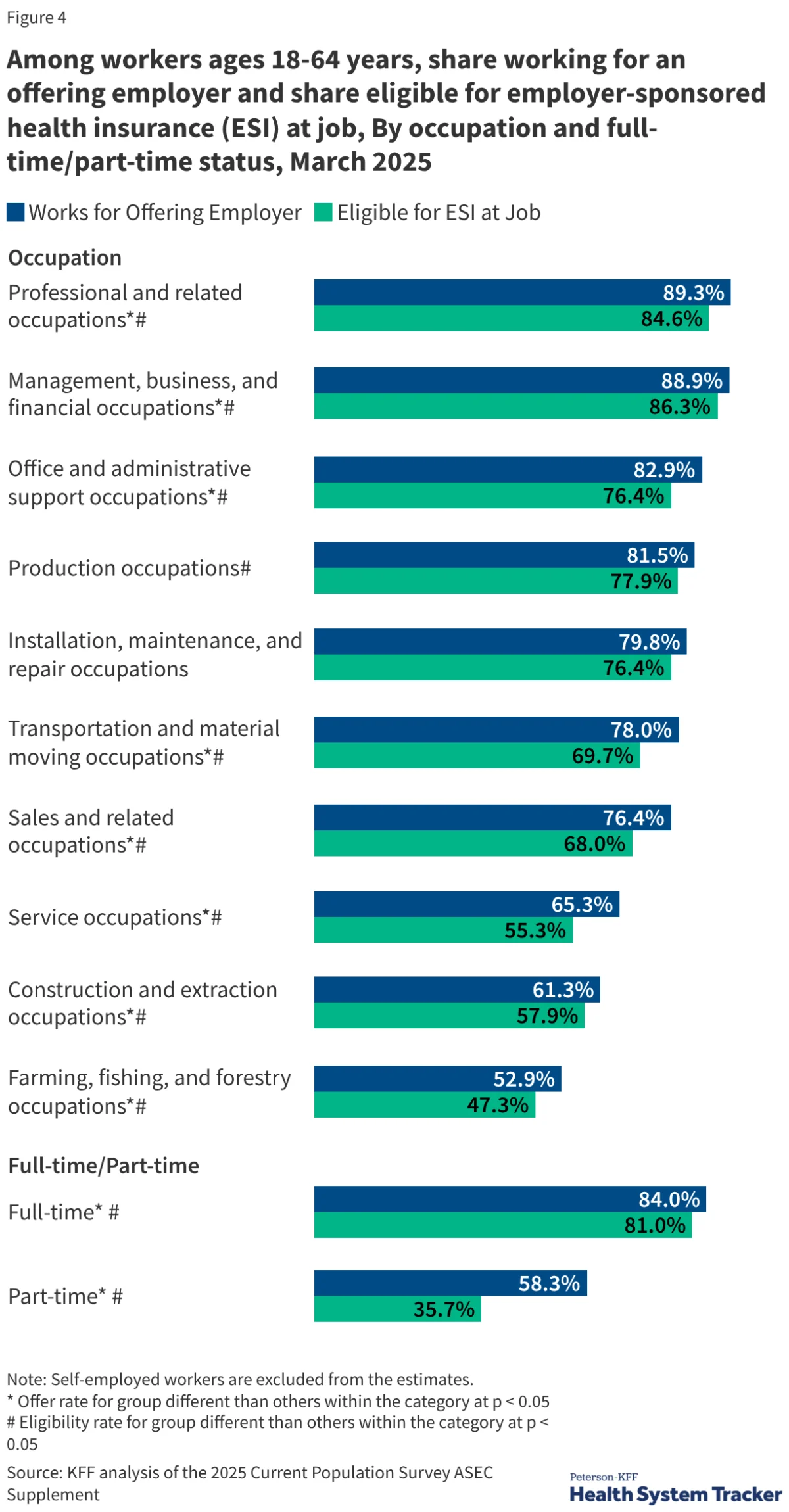

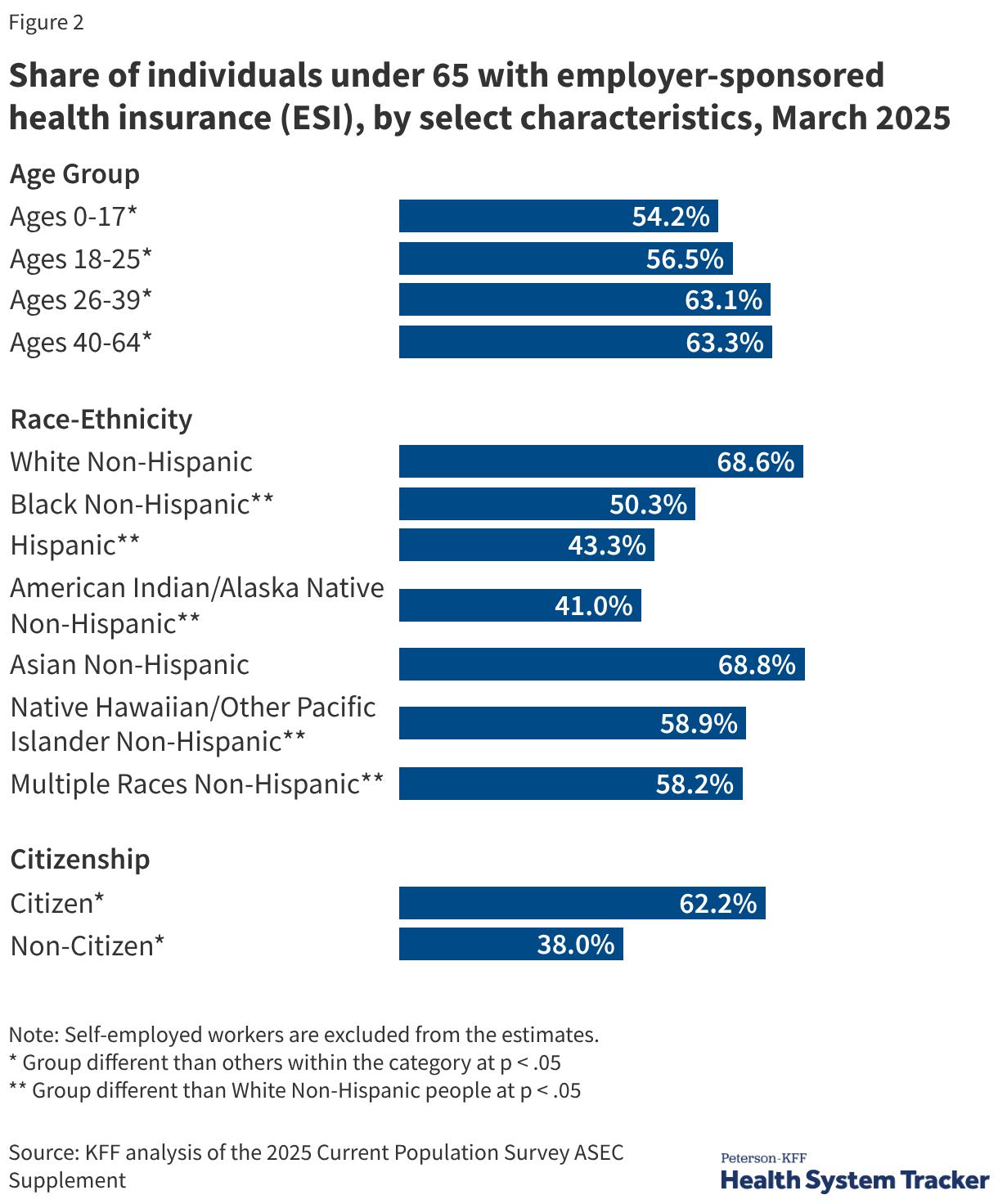

Disparities also persist across racial categories. Non-Hispanic White individuals are significantly more likely to have ESI compared to Hispanic, Black, and American Indian/Alaskan Native populations. These discrepancies often reflect broader systemic issues, including occupational segregation where minority populations are overrepresented in industries with lower rates of employer-sponsored benefits, such as agriculture, service, and construction.

The Rising Cost of Care: Premiums and Deductibles in 2025

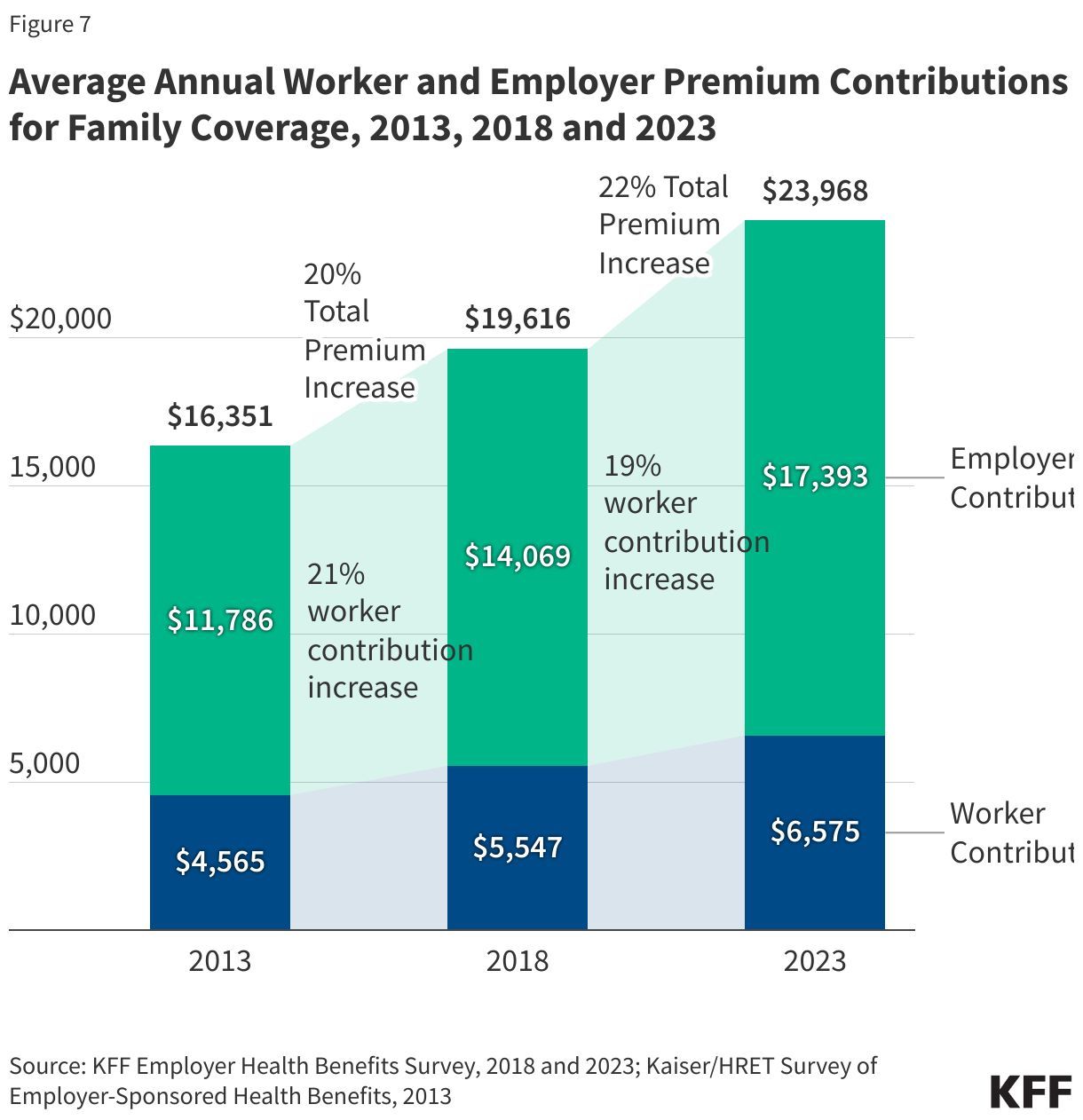

The cost of maintaining ESI has reached record highs. In 2025, the average annual premium for family coverage reached $26,993, while single coverage averaged $9,325. Over the last five years, family premiums have grown by 26%, a rate that mirrors inflation and wage growth but places a continuous strain on corporate and household budgets.

To manage these costs, employers have increasingly shifted the financial burden to workers through higher deductibles. In 2025, 88% of covered workers faced a general annual deductible. The average deductible for single coverage stands at $1,886, but workers at small firms face significantly higher burdens, averaging $2,631.

Analysts note that the surge in "High Deductible Health Plans" (HDHPs) has fundamentally changed the nature of health insurance. While these plans often include Health Savings Accounts (HSAs) to help enrollees save for medical expenses, they can create financial barriers to care. For low-income families, a $2,000 deductible may represent a significant portion of their liquid assets, potentially leading to the deferral of necessary medical services.

Strategic Plan Design and Network Management

In response to escalating costs, 2025 has seen a shift in how employers structure their provider networks. While the Preferred Provider Organization (PPO) remains the most common plan type, representing the majority of enrollees, there is a growing trend toward "narrow networks" and "tiered networks."

- Narrow Networks: Approximately 9% of firms now offer plans that limit the number of participating hospitals and physicians to those who meet specific cost and quality benchmarks.

- Tiered Networks: These plans encourage enrollees to use "high-performance" providers by offering lower cost-sharing (e.g., lower copays) for those in the top tier.

- Centers of Excellence: Many large employers now require or incentivise employees to travel to specific high-value facilities for complex procedures like spinal surgery or organ transplants.

Furthermore, price transparency rules enacted in recent years have begun to influence the market. Employers are increasingly using disclosed price data to negotiate better rates or to steer employees away from high-cost, low-quality providers.

Utilization Management and the Prior Authorization Debate

A significant point of contention in 2025 involves utilization management tools, specifically prior authorization. This process requires insurers to review and approve certain medical services or prescriptions before they are covered. While employers view this as a necessary tool to prevent inappropriate or wasteful spending, it has faced intense criticism from patients and providers.

A 2025 survey of large employers found that 44% of firms believe their employees have a moderate to high level of concern regarding the complexity of prior authorization. In response, several major insurers pledged in early 2025 to expedite these processes, though policy analysts remain skeptical about whether these voluntary measures will be sufficient to prevent care delays.

Implications and Future Outlook

The current state of employer-sponsored health insurance in 2025 presents a complex paradox. It is an efficient, tax-advantaged system that provides high-quality care to millions, yet it remains inaccessible or unaffordable for a significant portion of the working poor.

As the U.S. moves forward, several critical questions remain:

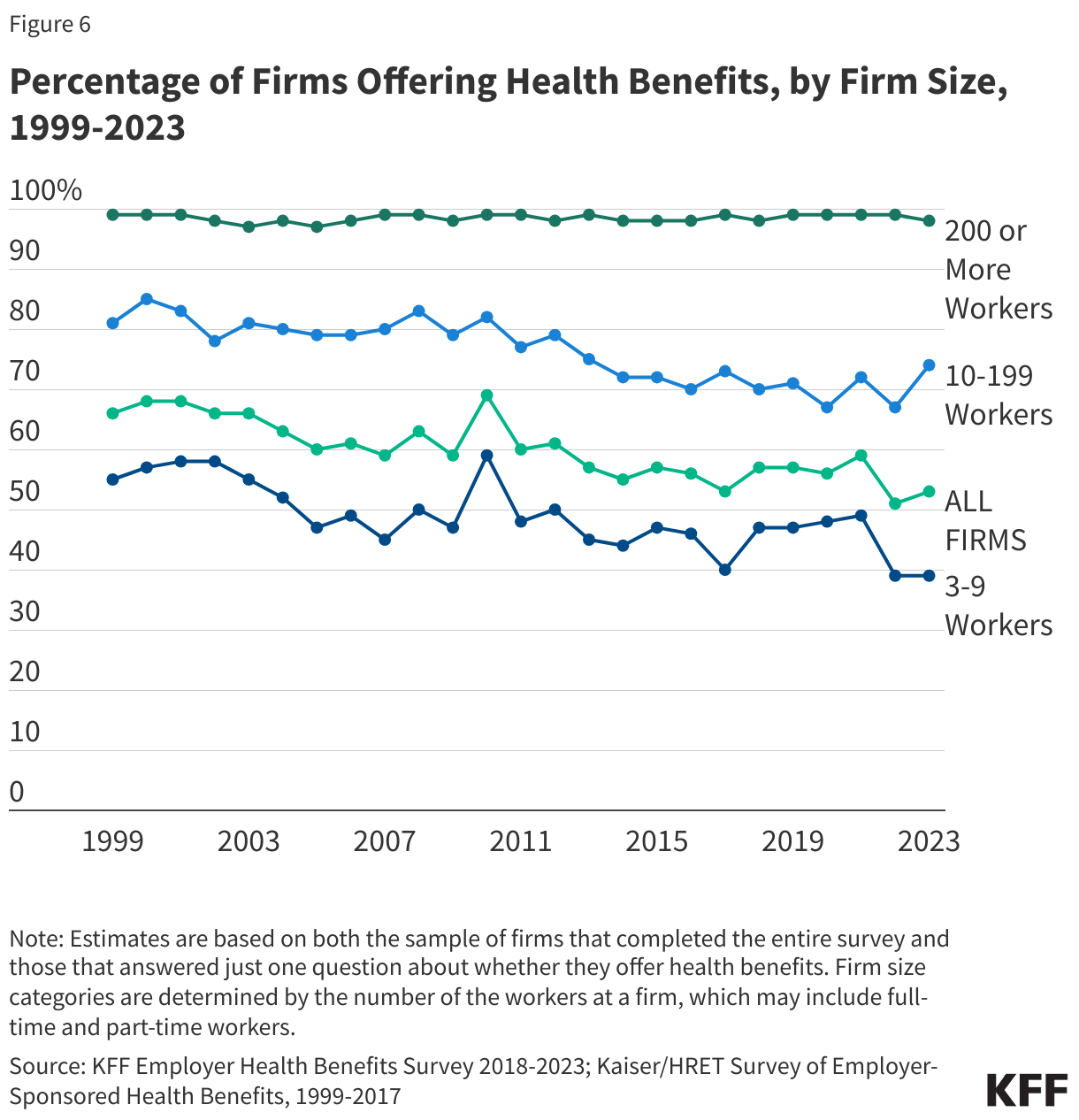

- Sustainability for Small Business: With only 51% of firms with 10-24 workers offering benefits, can small businesses continue to compete for talent without a more affordable entry point into the health insurance market?

- The Mental Health Gap: While 92% of firms believe their plans provide timely access to primary care, only 70% say the same for mental health services. Addressing this shortage remains a top priority for corporate benefits managers.

- Policy Shifts: The "family glitch" fix was a significant step toward affordability, but the core reliance on the $312 billion tax exclusion remains a subject of debate among economists who argue it contributes to "moral hazard" and over-consumption of healthcare services.

Ultimately, the future of ESI will depend on the ability of employers and insurers to innovate in network design and cost-sharing while ensuring that the most vulnerable segments of the workforce are not left behind in an era of rising medical costs. For now, the workplace remains the undisputed center of the American healthcare experience, for better or for worse.

{kind=link}