Health insurance benefits currently represent approximately 8% of total employee compensation in the United States, yet a stark divide persists in how these benefits are distributed and utilized across the socio-economic spectrum. A comprehensive analysis conducted by the Peterson-KFF Health System Tracker reveals that while employer-sponsored insurance remains the backbone of the American healthcare system, lower-wage workers face significant barriers to both access and enrollment. The study, which synthesized survey data and focus group insights from over 100 U.S. employers representing more than 250,000 employees, highlights a systemic gap: workers in lower-wage occupations are not only less likely to be offered health insurance by their employers but are also substantially less likely to enroll in coverage even when it is available to them.

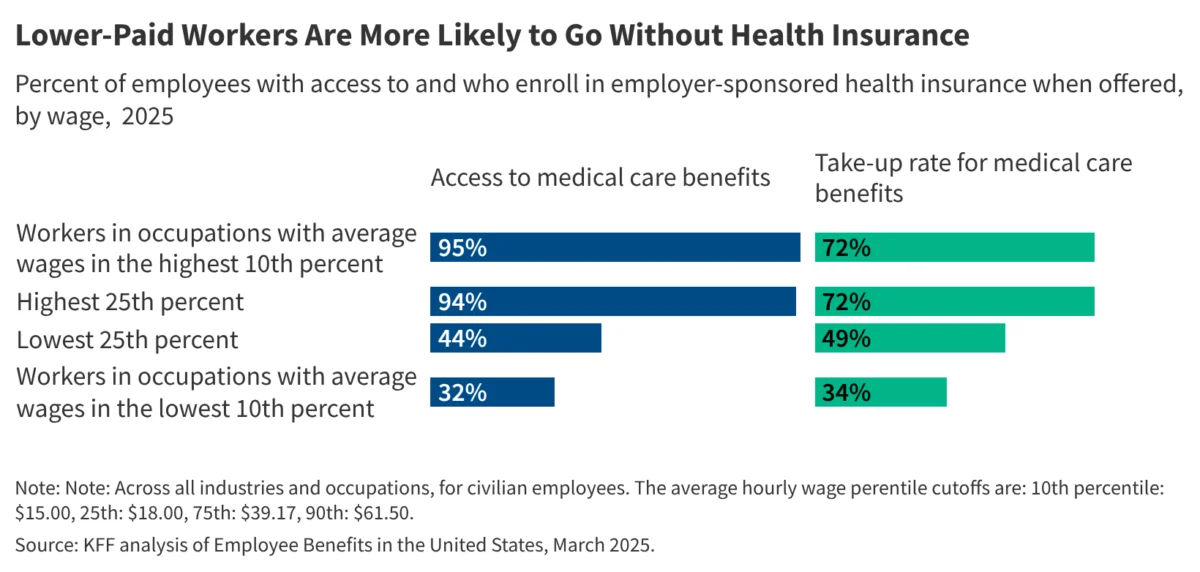

On average, approximately three out of four employees across the nation are offered health insurance through their workplace. Among those who are offered such benefits, nearly two-thirds choose to enroll. However, these aggregate figures mask a profound inequality. In higher-wage occupations, access to health benefits is nearly universal, with 94% of workers having the option to enroll. In contrast, only 44% of workers in lower-wage jobs—predominantly in the service, hospitality, and retail sectors—are offered health insurance through their employment. Furthermore, the "take-up" rate, or the percentage of workers who enroll once offered, shows a similar divergence. While 72% of higher-wage workers enroll in their employer’s plan, only 49% of lower-wage workers do the same, often due to the prohibitive cost of premiums and out-of-pocket expenses relative to their earnings.

The Economic Architecture of Employer-Sponsored Insurance

The current structure of the American labor market relies heavily on the "fringe benefit" model, where non-wage compensation like health insurance, retirement plans, and paid leave supplement hourly or salaried pay. According to the Bureau of Labor Statistics (BLS), health insurance is one of the most expensive components of an employee’s total compensation package. For employers, the cost of providing health insurance has risen steadily over the last two decades, outpacing both general inflation and wage growth. This has led many firms, particularly those operating on thin margins with large numbers of low-wage workers, to either limit eligibility or pass a larger share of the premium costs onto the employees.

The Peterson-KFF analysis underscores that for many lower-wage workers, the offer of insurance is "access" in name only. When a worker earning the federal minimum wage or slightly above is asked to contribute $150 to $200 per month toward a premium—in addition to facing high deductibles that can exceed $3,000—the benefit becomes an economic impossibility. This creates a cycle of under-insurance where the most vulnerable members of the workforce are forced to rely on emergency room care or forgo preventative treatments, ultimately leading to higher long-term costs for the healthcare system and decreased labor productivity.

A Historical Context of Workplace Benefits

The reliance on employers to provide health insurance is a uniquely American phenomenon that traces its roots back to the Second World War. During the war, the federal government imposed wage freezes to prevent inflation in a tight labor market. To attract workers without violating wage caps, companies began offering robust fringe benefits, including health insurance. In 1943, the Internal Revenue Service (IRS) ruled that employer contributions to group health insurance were tax-exempt, a decision codified by the Revenue Act of 1954.

This historical accident created a system where health security is inextricably linked to employment. While this functioned relatively well for the manufacturing-heavy economy of the mid-20th century, the shift toward a service-oriented and "gig" economy has exposed the flaws in this model. As the workforce bifurcated into high-skill, high-wage professional roles and low-skill, low-wage service roles, the disparity in benefits grew. The Peterson-KFF data is a contemporary reflection of this long-term structural divergence, showing that the "safety net" of employment-based insurance is increasingly failing those at the bottom of the income ladder.

Chronology of Policy Interventions and Market Shifts

The landscape of employer-sponsored insurance has been significantly shaped by several key milestones over the last fifteen years:

- 2010: The Passage of the Affordable Care Act (ACA): The ACA introduced the "employer mandate," requiring businesses with 50 or more full-time equivalent employees to offer affordable coverage or face penalties. While this increased the number of people offered insurance, it also led some employers to shift workers to part-time status (under 30 hours per week) to avoid the mandate.

- 2014-2018: Premium Stabilization and Deductible Growth: Following the implementation of ACA exchanges, employer-sponsored premiums began to stabilize, but deductibles surged. This era marked the rise of "High Deductible Health Plans" (HDHPs), which lowered monthly premiums but increased the financial burden on workers at the point of care.

- 2020-2022: The COVID-19 Pandemic: The pandemic highlighted the volatility of employer-linked insurance. Millions of workers lost coverage during lockdowns. Conversely, the labor shortage that followed forced some employers in low-wage sectors to offer better benefits to attract talent, though the Peterson-KFF data suggests these gains were not universal.

- 2023-Present: The Inflationary Pressure: Rising costs of medical services and prescription drugs have put renewed pressure on employer budgets. Employers are currently grappling with how to maintain benefits without eroding their bottom line, often resulting in "skinny plans" that offer limited coverage for lower-wage tiers of the workforce.

Insights from the Focus Groups: The Employer’s Dilemma

The Peterson-KFF study included focus groups with over 100 employers, providing a qualitative look at why these disparities persist. Many employers in the service and retail industries expressed a desire to provide better coverage but cited the "affordability cliff" as a primary obstacle. For a company employing thousands of hourly workers, even a small increase in the employer’s share of the premium can result in millions of dollars in additional annual expenses.

Employers also noted that lower-wage workers often prioritize immediate take-home pay over deferred benefits. In focus group sessions, managers reported that many employees opt out of insurance because they cannot afford the payroll deduction, even if the employer is subsidizing 70% or 80% of the total cost. Furthermore, some lower-wage workers may qualify for Medicaid or subsidies through the ACA marketplace, which can sometimes provide more comprehensive coverage at a lower cost than their employer’s plan, leading to lower enrollment rates within the company.

Supporting Data: Comparing the Wage Tiers

The gap in coverage is most visible when looking at the specific occupations cited in the analysis. Higher-wage jobs, including those in management, engineering, and legal services, see nearly universal offering rates. In these sectors, health insurance is viewed as a standard part of the "total rewards" package necessary to compete for specialized talent.

In contrast, service occupations—such as food preparation, building maintenance, and personal care—show the lowest rates of both offering and enrollment. According to supplementary data from the KFF Annual Employer Health Benefits Survey, the average annual premium for family coverage reached nearly $24,000 in 2023, with workers on average contributing over $6,500. For a worker earning $30,000 a year, contributing $6,500 toward a premium represents more than 20% of their gross income, a figure that the federal government deems "unaffordable" under ACA guidelines (which currently set the threshold at approximately 8.39% of household income).

Analysis of Implications for Public Health and the Economy

The implications of these findings extend far beyond the corporate balance sheet. When a large segment of the workforce lacks access to affordable health insurance, the consequences are felt throughout the broader economy and public health infrastructure.

1. Increased Reliance on Public Safety Nets:

When employers do not provide affordable coverage, the burden shifts to the public sector. Many lower-wage workers turn to Medicaid (in states that expanded it) or the ACA marketplace. This effectively means that taxpayers are subsidizing the labor costs of private companies that do not provide adequate benefits.

2. Medical Debt and Financial Instability:

For the 51% of lower-wage workers who are offered insurance but do not enroll, a single medical emergency can lead to catastrophic financial ruin. Medical debt remains the leading cause of bankruptcy in the United States. Even for those who do enroll, high deductibles often mean they are "under-insured," possessing a card but unable to afford the cost of using it.

3. Labor Market Friction:

The disparity in benefits creates "job lock," where workers are afraid to leave a position because of the risk of losing health coverage, or conversely, it prevents workers from entering certain sectors because the lack of benefits makes the total compensation package unviable. This reduces labor mobility and can stifle economic growth.

4. Public Health Outcomes:

Lower-wage workers are more likely to have chronic conditions such as diabetes or hypertension, which require consistent management. Lack of insurance leads to "episodic care"—seeking treatment only when a condition becomes acute. This is the most expensive way to manage health and leads to poorer long-term outcomes and higher mortality rates among lower-income populations.

Official Responses and Future Outlook

Industry groups and policymakers have reacted to these disparities with a variety of proposed solutions. Some business advocacy groups argue for more flexibility in the types of plans they can offer, including the expansion of Association Health Plans (AHPs) that allow small businesses to band together to purchase insurance. However, critics argue that these plans often circumvent the "essential health benefits" required by the ACA, leading to lower-quality coverage.

On the legislative front, there are ongoing discussions regarding the "family glitch" fix and the permanent extension of enhanced ACA subsidies, which aim to make non-employer coverage more affordable for those whose workplace options are too expensive. Some policy analysts suggest a shift toward "decoupling" health insurance from employment entirely, moving toward a more universal system that would treat health coverage as a public utility rather than a workplace perk.

The Peterson-KFF Health System Tracker analysis serves as a critical reminder that the current trajectory of the U.S. health system is one of widening inequality. As healthcare costs continue to consume a larger portion of the American GDP, the divide between those who can afford to stay healthy and those who cannot is likely to sharpen. For the millions of service workers who keep the economy running, the promise of employer-sponsored health insurance remains an elusive or unaffordable prospect, highlighting the need for continued reform in how the nation values and protects the health of its entire workforce.

{kind=link}